Mortgage-backed securities (MBS) may seem complex at first, but they are an essential part of the financial world and can offer investors unique opportunities. These securities are created by pooling together a large number of individual home loans into a single investment product, which is then sold to investors. The payments made by homeowners on these mortgages are distributed to the investors, allowing them to earn returns from the interest and principal payments.

For investors seeking diversification and income, MBS can be an attractive option. However, it’s important to understand how these securities work and the risks involved before making them a part of your investment strategy.

What Are Mortgage-Backed Securities?

Mortgage-backed securities are a type of bond that is backed by home loans. When a bank or lending institution issues a mortgage, it often sells that loan to a government-sponsored entity, such as Fannie Mae, Freddie Mac, or a private institution. These institutions then bundle hundreds or thousands of these loans together to create a mortgage-backed security. Investors can buy shares in these securities, and in return, they receive regular payments based on the monthly mortgage payments made by homeowners.

The key feature of MBS is that they are backed by real assets—homes. As long as the homeowners continue to make their mortgage payments, investors will receive their share of those payments. The payments include both the principal (the amount borrowed) and the interest, providing a steady stream of income for investors.

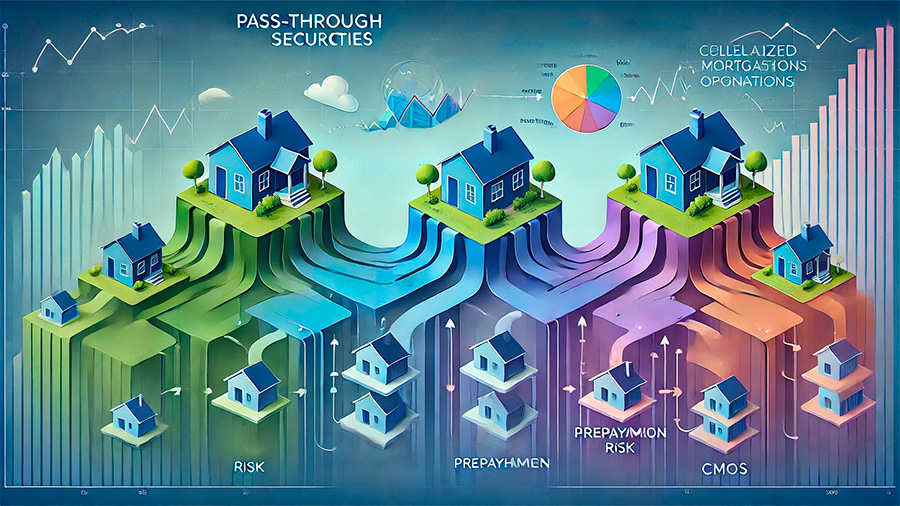

Types of Mortgage-Backed Securities

There are two main types of mortgage-backed securities: pass-through securities and collateralized mortgage obligations (CMOs).

Pass-through securities are the simpler and more common type. In these securities, payments made by homeowners on their mortgages are collected by the issuer and then passed directly to the investors, minus a servicing fee. Investors receive monthly payments that reflect both principal and interest, and the amount they receive depends on the portion of the MBS they hold.

Collateralized mortgage obligations (CMOs) are more complex and divide the mortgage payments into different classes, or “tranches.” Each tranche has different risk levels, and the payments are structured so that some investors receive their returns earlier, while others take on more risk for potentially higher returns. This makes CMOs more flexible, but also more complicated.

How MBS Generate Returns

When you invest in a mortgage-backed security, your returns come from the payments homeowners make on their mortgages. As a homeowner makes monthly payments, part of that payment goes toward paying down the principal of the loan, and part goes toward the interest. These payments are collected by the issuer of the MBS and distributed to investors based on their share of the security.

One advantage of MBS is that they provide regular, predictable income. Since homeowners typically make monthly mortgage payments, investors in MBS can expect steady returns, which makes these securities appealing for those looking for income-generating investments, such as retirees or income-focused portfolios.

However, mortgage-backed securities also carry risks, especially in terms of how much interest and principal will be repaid and when. A key risk is “prepayment risk,” which occurs when homeowners pay off their mortgages early, either by refinancing or selling their homes. This can reduce the total amount of interest that an investor was expecting to receive over the life of the MBS.

Benefits of Investing in Mortgage-Backed Securities

Mortgage-backed securities offer several potential benefits for investors:

- Steady income: MBS can provide a consistent income stream, especially when interest rates are stable, making them appealing for investors looking for regular cash flow.

- Diversification: Since MBS are backed by real estate, they offer a way for investors to diversify their portfolios by including exposure to the housing market without owning physical property. This can help spread risk across different asset classes.

- Government backing: Many mortgage-backed securities are issued by government-sponsored entities like Fannie Mae and Freddie Mac, providing a layer of security. These GSE-backed MBS are considered relatively low-risk because they are supported by government guarantees.

For investors, these benefits can make MBS a reliable addition to a well-rounded portfolio. The steady income and diversification opportunities are particularly attractive during times of economic stability when default rates on mortgages are low.

Risks Associated with MBS

While mortgage-backed securities offer several benefits, they also come with risks that investors should be aware of.

- Prepayment risk: One of the primary risks of MBS is that homeowners may choose to pay off their mortgages early, particularly when interest rates drop. This early repayment reduces the amount of interest that investors would have otherwise earned over the life of the mortgage. When many homeowners refinance or sell their homes, MBS investors receive less interest income than anticipated.

- Interest rate risk: MBS are sensitive to changes in interest rates. If interest rates rise, new MBS may offer higher returns, making older ones less attractive to investors. This can reduce the market value of existing MBS, especially if the investor needs to sell the security before it matures.

- Credit risk: While government-backed MBS are considered relatively safe, private-label MBS (those issued by private institutions) carry more credit risk. If homeowners default on their mortgages, investors in private-label MBS could see reduced returns or losses.

Understanding these risks is essential for managing an MBS investment effectively. Investors need to weigh the benefits of steady income against the possibility of prepayment or credit-related issues, especially in volatile economic environments.

Adding MBS to Your Portfolio

For investors looking to diversify their portfolios, mortgage-backed securities can be a valuable addition. Their steady income, diversification benefits, and relatively low correlation to stock market performance make them a useful tool for balancing risk across asset classes. However, because of the inherent risks, especially related to interest rates and prepayments, MBS are often better suited for investors with a longer time horizon and a good understanding of bond markets.

Investors can access MBS through mutual funds or exchange-traded funds (ETFs) that specialize in mortgage-backed securities, making it easier to diversify across multiple MBS without purchasing them individually. These funds also provide professional management, which can help mitigate some of the risks associated with prepayment and interest rate fluctuations.

Conclusion

Mortgage-backed securities provide a way for investors to tap into the housing market while earning a steady stream of income. Though they come with specific risks, such as prepayment and interest rate risk, MBS can be a profitable addition to a diversified portfolio when managed carefully. By understanding how MBS work and how they fit into a broader investment strategy, investors can make informed decisions that support their long-term financial goals.